If a business is paying hundreds of thousands of dollars in premiums for workers’ compensation, general liability, and commercial auto insurance, chances are they are considering alternatives such as captive insurance — or they will be soon.

For many independent insurance agents, this is where the uncertainty begins. Captive insurance can seem complex, and agents fear they will no longer have a relationship with their clients once those clients are enrolled in the captive program.

A casualty group captive offers a different approach. It allows businesses with strong loss histories and at least $250,000 in annual casualty premiums to insure their casualty risks through a member-owned insurance company while keeping the independent agent at the center of the client relationship.

This guide explains how casualty group captives work, what businesses qualify, how risk sharing and reinsurance function, and how agent-focused captive programs differ from traditional captive managers.

What Is a Casualty Group Captive?

A casualty group captive is a member-owned insurance company formed by businesses with similar views about risk management. Members pool their resources to insure their own general liability and workers' compensation risks, rather than purchasing guaranteed-cost insurance from a traditional carrier. "Casualty" refers to the core lines: general liability, workers' compensation, and often commercial auto. Your client stops being just a policyholder and becomes a co-owner of the insurance entity covering their risk.

Rather than sending underwriting profits to a commercial insurance carrier, members may receive underwriting profits and investment income back when the captive performs well.

For qualifying businesses, this creates greater pricing stability, improved transparency, and more control over long-term insurance costs.

Casualty Group Captive vs. Traditional Insurance

|

Traditional Insurance |

Casualty Group Captive |

|

Carrier owns underwriting profit. |

Members own underwriting profit. |

|

Premiums driven largely by market cycles |

Pricing reflects member performance. |

|

Limited financial transparency |

Members see claims, reserves and financial performance. |

|

Carrier keeps investment income. |

Members benefit from investment returns. |

|

Renewal surprises are common. |

Performance is monitored throughout the year. |

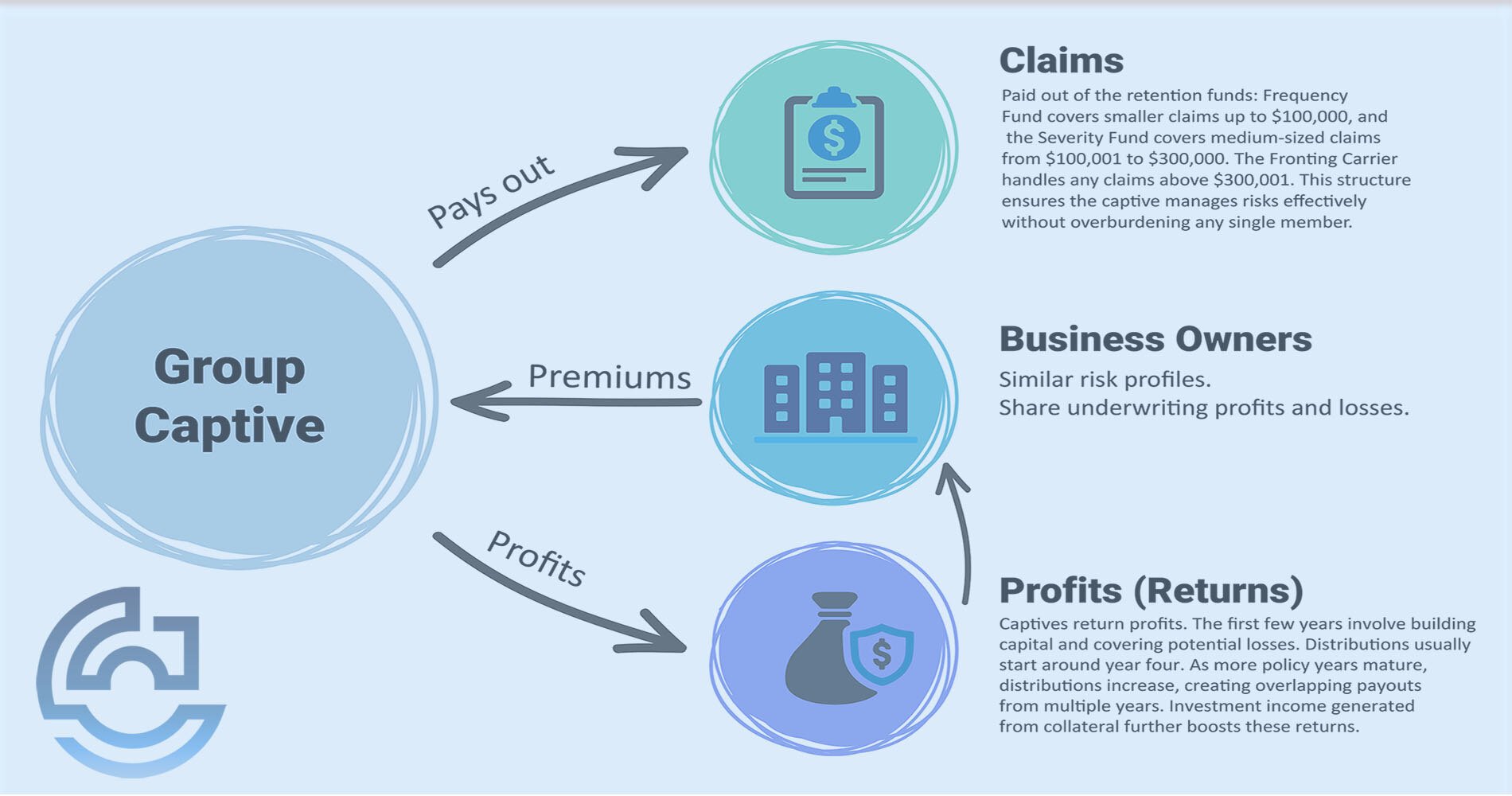

How Does the Member-Owned Structure Work?

Multiple businesses collectively own the insurance subsidiary. Each contributor pays premiums based on their risk profile, sharing in underwriting results and investment income. The structure is set up as follows: members retain small, predictable losses; the group shares medium risks; and reinsurance covers catastrophic losses. Most captives have a board drawn from the membership, so your client has a voice in operations, coverages, and surplus allocation.

What Role Does Reinsurance Play?

Reinsurance protects the group from catastrophic losses. Most captives buy excess coverage above the retention layer, transferring large or aggregated claims to A.M. Best-rated carriers — alternative risk transfer without the exposure of full self-insurance.

Fronting Arrangement

A fronting carrier issues policies on the captive's behalf and handles state regulation, because captives aren't admitted carriers. The captive reinsures the fronting carrier for the agreed retention layer. This ensures the client receives compliant policies and certificates while benefiting from the captive structure.

Lines of Coverage Included

- Workers' Compensation: Usually the largest line. Members retain a portion up to a threshold; the group shares the mid-level; and the excess reinsurance covers catastrophic claims.

- General Liability: Protects against third-party bodily injury/property damage. Captive Coalition's GL Captive program targets accounts with $250,000+ across core lines.

- Commercial Auto Liability: Often folded into the same quota-share model, typically up to a $500,000 retention layer.

What Businesses Qualify?

To determine if a client fits in a captive, agents should ask three questions:

- Do they have $250,000+ in annual casualty premiums across WC, GL, and auto?

- Do they possess a clean-to-moderate loss history?

- Do they have the financial stability for upfront capitalization and collateral?

In our conversations with agents, the most common hurdle isn't loss history — it's insufficient premium volume.

How Pricing Differs From Traditional Insurance

Traditional guaranteed-cost plans transfer all risk to the carrier, which keeps profit and investment income regardless of a client’s safety record. In a group captive, premiums reflect the client's own performance. Safe operations return financial benefits to the member, with full visibility into where every premium dollar goes.

Financial Benefits of Captive Insurance

- Premium Stability: Pricing reflects the client's actual loss experience rather than market swings.

- Profit Potential: Strong group performance returns underwriting profit and investment income to members.

- Long-Term Control: Members actively shape governance, claims philosophies, and safety standards.

What Commitments Are Required?

Joining a captive is not a short-term trial. Most programs expect a five- to seven-year commitment, so the captive can allow loss data to mature. Collateral requirements are real. Members post funds to secure their retention layer, which is tied up during the commitment period and returned as losses close out. For example, a manufacturer with $350,000 in annual casualty premium might post collateral equal to a percentage of expected losses. Renewal-only members tend to underperform.

Risk Sharing and Vetting

Because members share both good and bad financial results, rigorous risk selection matters. Strict underwriting keeps out high-risk businesses that would drag down the group performance.

- Heterogeneous Captives: A mix of industries together to diversify risks.

- Homogeneous Captives: Focus on a single industry to build specialized coverages but concentrate risks.

Keeping the Independent Agent at the Center

With many programs, your role changes when the client signs. One misconception is that when a client joins a captive, the agent loses the client relationship — it doesn't have to. As an agent-focused program, you remain the quarterback. Client questions come to you, you bring them to the captive team, and answers route back through you. This keeps you in control and reassures clients of your ongoing support.

How to Introduce Captives to Clients

Lead with curiosity rather than conviction. Ask questions about their current spend and satisfaction with risk management, rather than pushing a hard sale. You do not need to be the captive expert; you need to be the trusted advisor confident enough to start the conversation. For technical background, you can reference resources from CICA, IRMI, NAIC, and A.M. Best.

Conclusion

A casualty group captive is a member-owned program that enables well-run businesses to take control of their Workers’ Compensation and General Liability insurance costs — sharing risk across a vetted group, retaining underwriting profit, and gaining transparency. The challenge isn't whether the captive model works; it is making sure you feel equipped to raise the option without losing your client.

Your role as an independent agent is crucial for evaluating fit and guiding the conversation. A good next step is checking a client against the qualification criteria above. Captive Coalition helps agents evaluate fit and run that conversation while staying at the center of the relationship.

Frequently Asked Questions

Is a casualty group captive the same as self-insurance?

No — self-insurance means retaining your own risk; a group captive shares risk among vetted members and reinsures catastrophic losses.

What minimum premium qualifies?

$250,000+ in combined limits across General Liability, Workers’ Compensation, and Commercial Auto.

What industries commonly join?

Well-run construction, manufacturing, distribution, transportation, and similar operations.

How much collateral is required?

Varies by program, typically a percentage of expected losses; returns as claims close out.

How long does placement take?

Usually 60–90 days.

Can my client exit?

Yes, but five-to-seven-year commitments and tied-up collateral mean early exits can forfeit benefits.

Does joining affect my commission?

Captive Coalition protects agent relationships and keeps you involved throughout the process.

How are claims handled?

Through the fronting carrier and captive administrator, with member visibility.

It's always your client. Never ours.

{kind=link}