Group captive insurance offers your clients something the traditional market cannot: the chance to become owners of their own insurance company. This structure helps your clients keep underwriting profit, earn investment income, and manage their risk, rather than subsidizing less-disciplined insureds.

For independent insurance agents, understanding how group captives build long-term client value can set you apart. Captive Coalition helps agents confidently present these programs to their best clients. This article explains the key mechanisms—underwriting profit, surplus distributions, and disciplined risk management—that create lasting financial benefits.

Key Takeaways: How Group Captive Insurance Creates Long-Term Client Value

- Underwriting profit stays with member-owners rather than going to a traditional carrier, creating direct financial returns for your clients.

- Surplus distributions reward disciplined risk management, often returning unused loss funds to members after claims are settled.

- Premium stability protects your clients from market volatility since their rates are based on their own loss history, not industry averages.

- Captive Coalition gives independent agents the training and resources to recommend group captives to qualified clients confidently.

- Stronger client relationships develop when you help clients control costs and improve safety outcomes year after year.

What Is Underwriting Profit in a Group Captive?

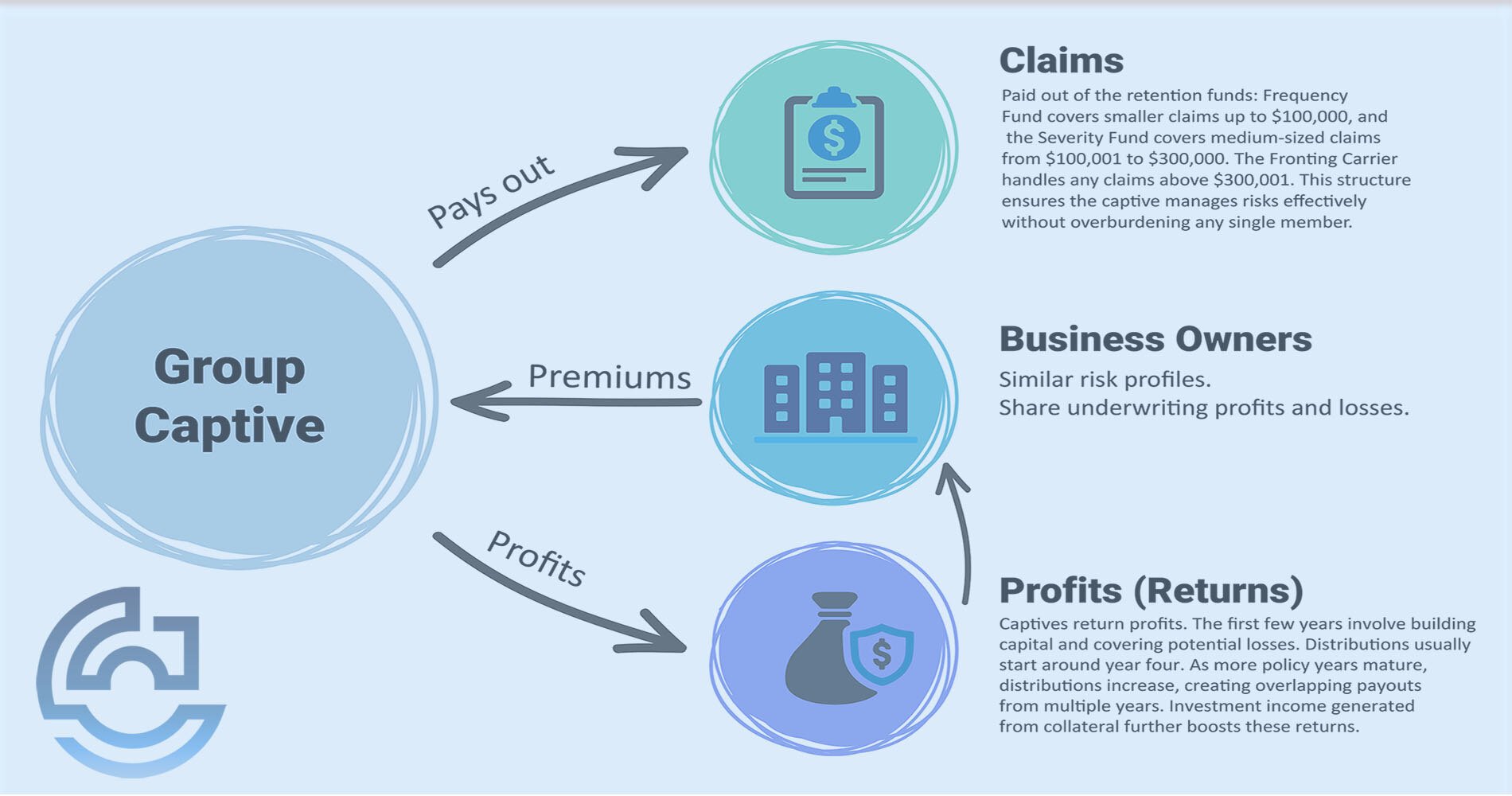

Underwriting profit is the money left over after losses and expenses are paid from collected premiums. In a traditional insurance arrangement, the carrier keeps this surplus. In a group captive, it belongs to the members.

This ownership structure changes everything. Your clients stop being premium payers and start owning their own insurance companies. When claims come in lower than expected, that difference flows back to them—not to a distant shareholder.

According to research from the Insurance Information Institute, captive insurers consistently outperform the commercial sector in key financial measures, including operating ratios. This means more dollars stay in the hands of member-owners over time.

How Do Surplus Distributions Work in Group Captives?

Surplus distributions are the mechanism by which unused loss funds are returned to members. When your client manages risk well and keeps claims low, those reserved dollars eventually come back as dividends.

The timing depends on the line of business. Property claims with minimal liability may allow distributions in six to twelve months. Liability claims have longer development periods, with payouts sometimes occurring three to five years after the policy year ends.

This creates a compounding effect. Each year your client performs well, more surplus accumulates. Over multiple years, these distributions can significantly reduce the total cost of risk—often by 28% or more in the first three years for clients with stable loss histories.

Why Does Disciplined Risk Management Matter for Group Captive Success?

Group captives only admit businesses that demonstrate strong safety programs and favorable loss histories. This selectivity protects all members from subsidizing poor performers—a stark contrast to the traditional market.

Once inside, members are incentivized to maintain or improve their safety standards. Better safety means fewer claims, which translates directly to higher surplus distributions and lower future premiums.

This creates a virtuous cycle. Your clients improve their workplaces, reduce injuries, and see financial rewards. Their employees benefit from safer conditions. And you, as their agent, become the trusted advisor who helped make it happen.

How Group Captives Reduce Premium Volatility for Your Clients

Traditional insurance premiums fluctuate based on industry-wide losses, carrier appetites, and market cycles. Your client can have an excellent year and still face a significant rate increase because other insureds performed poorly.

Group captives work differently. Each member's premium is based on their own five-year loss history and risk profile. This means your best clients—the ones with strong safety cultures—pay rates that reflect their actual performance.

This stability helps clients budget more accurately. They can plan capital investments, hiring decisions, and operational changes without worrying about surprise premium spikes. That predictability has real business value beyond just the insurance cost itself.

Why Experienced Agents Revisit Group Captives Later in Their Careers

Many agents learn about captives early but hesitate to recommend them. The concepts seem unfamiliar, and guaranteed cost programs feel safer to discuss. Years later, these same agents often come back to captives.

The reason is simple: experience reveals the limitations of guaranteed cost insurance. Agents watch good clients get penalized by market hardening. They see renewal increases that bear no relationship to their client's actual performance.

Captive Coalition works with experienced agents who want to offer their best clients something better. The training and resources for independent agents make it easier to have these conversations with confidence—and to protect the client relationships you have built over decades.

What Happens When Your Client Shifts From Guaranteed Cost to a Group Captive?

The shift from guaranteed cost to group captive ownership involves a mindset change. Your client moves from buying a product to owning an insurance company alongside other safety-conscious businesses.

This ownership brings responsibilities: attending board meetings, participating in governance, and maintaining the safety standards that earned them admission. For the right clients, these are features, not burdens.

The financial transition also requires planning. Collateral requirements exist and are typically paid over multiple years. But the potential returns—underwriting profit, investment income, and reduced premiums—often far exceed these upfront commitments for qualified participants.

In Conclusion: Building Long-Term Client Value With Group Captive Insurance

Group captive insurance creates long-term client value through three interconnected mechanisms. Underwriting profit remains with member-owners rather than flowing to traditional carriers. Surplus distributions reward disciplined risk management year after year. And premium stability gives your clients predictability that the traditional market simply cannot match.

For independent agents, presenting group captives to qualified clients strengthens relationships and protects your book of business. Captive Coalition equips you with the education and support to have these conversations confidently—helping you serve your best clients while building your own revenue.

FAQs About How Group Captive Insurance Creates Long-Term Client Value

What qualifies a client for group captive membership?

Clients typically need a strong safety culture, a favorable five-year loss history, and financial stability. They should be paying at least $200,000 in combined general liability, auto, and workers' compensation premiums annually.

Captive Coalition helps agents assess client qualifications through our captive assessment tool, making it easier to identify which accounts are ready for this conversation.

How long until my client sees financial returns from a group captive?

Financial returns begin accumulating immediately through investment income on premiums and collateral. Surplus distributions typically start after the third year, once underwriting years close.

The compounding effect grows stronger over time. Clients who maintain good loss experience often see their total cost of risk drop significantly by year four or five.

Will I lose control of my client if they join a group captive?

No. Captive Coalition operates under five non-negotiable rules that protect agent relationships. Your client remains your client—there are no surprise broker-of-record changes or competition for your business.

This agent-first approach means you can confidently recommend captives, knowing your relationship stays intact.

What happens if my client has a bad claims year in the captive?

A single bad year does not disqualify a client or wipe out previous gains. Group captives are structured to handle normal claims variation through reinsurance and shared risk pools.

However, a pattern of poor performance can lead to higher future premiums or membership review. This accountability mechanism protects other members and encourages ongoing risk management discipline.

How does Captive Coalition support independent agents selling group captives?

Captive Coalition offers training, resources, and ongoing support specifically designed for independent agents. This includes educational materials, client presentation tools, and access to experienced advisors who can answer technical questions.

The goal is to make captive insurance accessible so you can confidently serve your best clients without needing to become a captive expert yourself.

Topics:

{kind=link}